July 10, 2025

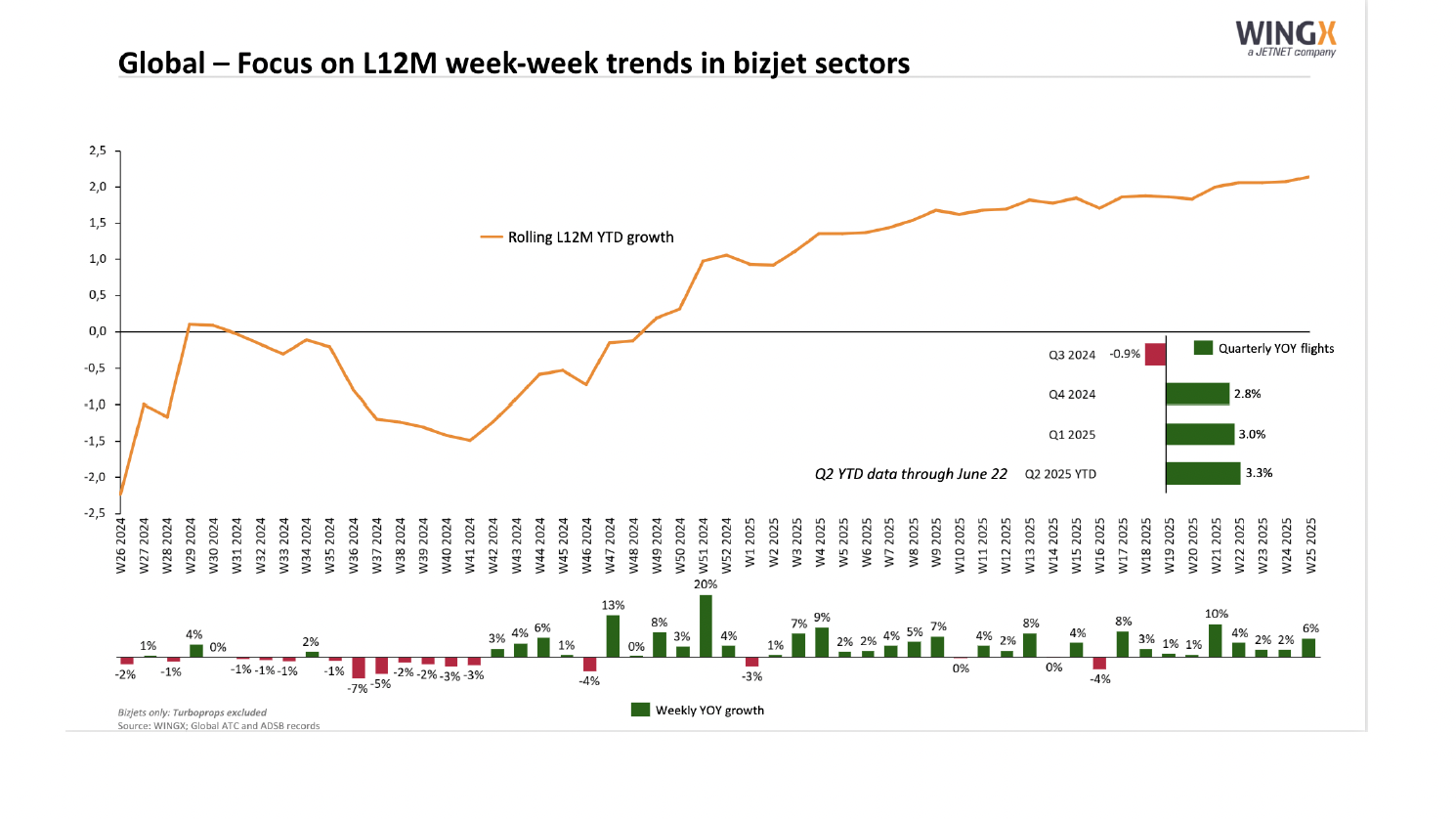

The recovery in private jet traffic at this point appears to be hitting a ceiling of around 85% compared to 2019. That’s the assessment from Wing-X weekly’s global tracking report.

And while that sounds good compared to other sectors of the travel industry, it equates to a reduction of about 50,000 fewer private aviation sectors since the start of September. Including private jets and turboprops. In terms of hours, just over 550,000 hours have been operated in that period, an 18% year-over-year drop.

“It’s encouraging that the recovery has not significantly relapsed as we move from Summer to Autumn, despite much less support from leisure travelers,” said Richard Koe, managing director of WingX.

He added, “The U.S. market is behind the European curve on the pandemic, with opening-up in Florida now releasing pent-up demand, whereas the Northeast is still restricted and activity well below normal. European activity shows more signs of wilting now we´re out of the summer season, but as in the U.S., the charter market is continuing to be relatively resilient.”

In terms of what type of aircraft are doing better, in Europe, smaller is beautiful. Turboprops flights are down by 11% versus a 19% decline in North America.

Around-the-word, private aviation activity above 90% of normal in Asia, although flight hours are down 28%, indicating few long-haul flights. Flight hours are trending down slightly in South America and Oceania, and by almost 20% in Africa, but sectors are actually up YOY in all three regions in the last four weeks, according to WingX.

For the U.S., WingX says the 7-day rolling trends reached its highest point since mid-March, just over 7,900 sectors flown daily in the first week of October. That compares with 2,500 daily sectors during the April low point.

Bright spots in the U.S. were Colorado and Florida, each up by more than 5% versus last year. Activity out of Arizona and South Carolina was on par with 2019.l. But demand in three of the most important markets, Texas, California, and New York was 15% to 20% below normal. Flight activity in New Jersey, where Teterboro was previously the country’s busiest private jet airport, continues to stagnate at 50% below normal.

Across the U.S., demand continues to favor smaller private jets. Very light and light jet segments were at 90% of normal. Super-mid and midsize jets are 15% under, but turboprop fell 20%. Ultra-long-range sectors are down 23% with flight hours down by 36%.

There was variation within segments, with single-digit declines for Phenom 300, Nextant, Citation Ultra, Citation CJ4, and Pilatus PC-12 activity. Across the whole fleet, Part 135 demand was most buoyant, trending 11% below since August, and just 5% down in hours. Part 91 activity was dulled by lacking business travel, down 25%.

Find the perfect solution for your private aviation needs

Save Time. Buy Confidently.

Receive an apples-to-apples comparison of programs that meet your needs from more than 500 jet card and fractional options covering 65 points of differentiation and over 40,000 data points.