August 21, 2025

Double-digit YOY gains in Florida and California helped power worldwide private jet flight activity to a 5% YOY gain in Week 31.

Worldwide private jet flight activity (74,850 segments) continued its upward trend in Week 31 with 5% year-over-year growth.

Sequentially, private jet segments globally dipped 2% for the week ending August 3, 2025.

So far, on a year-over-year basis, the scorecard shows:

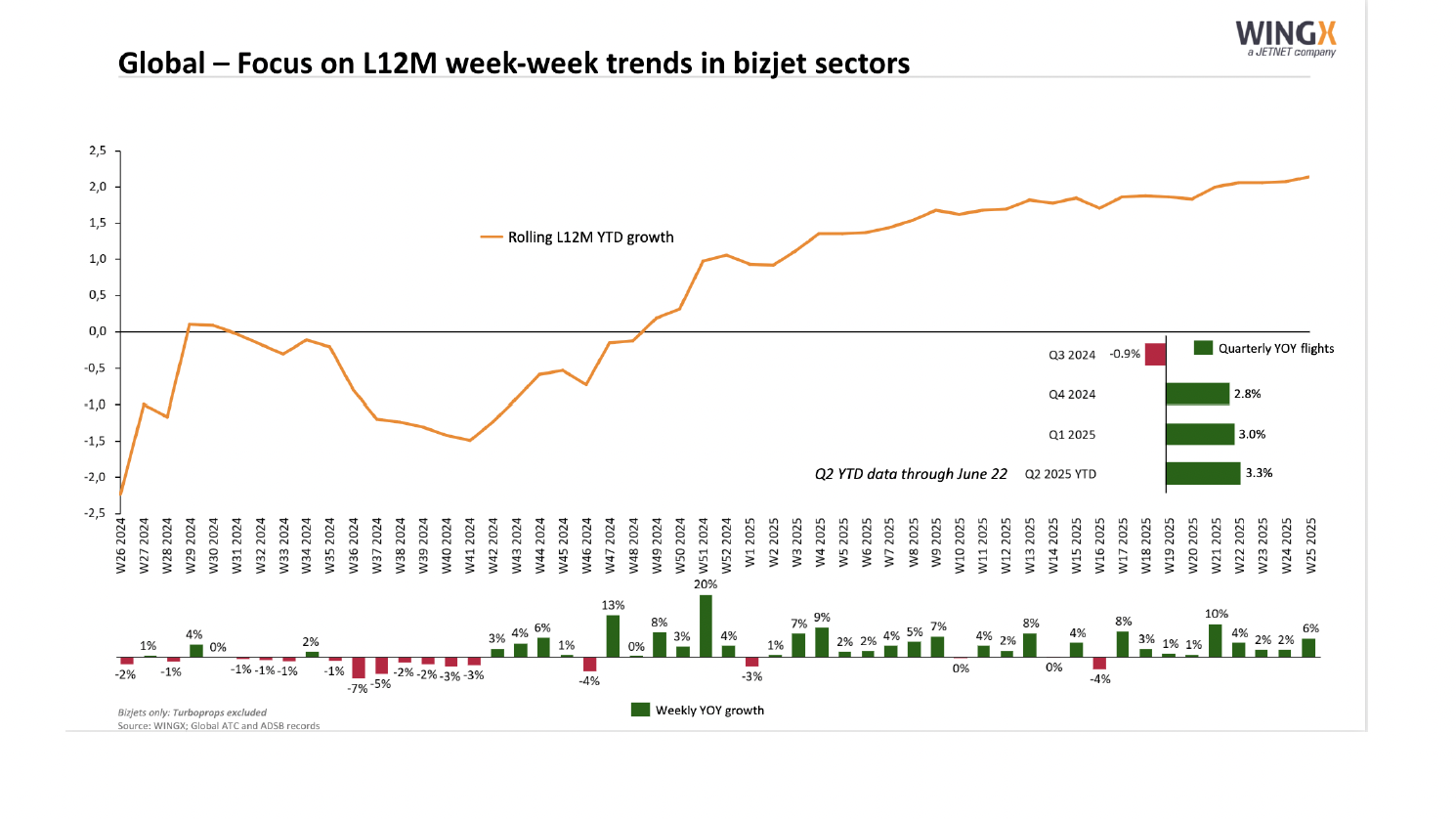

For July, segments increased 3.1% to 331,768 flights year-over-year.

What’s more, July flights were up 4.2% compared to July 2023.

The global active private jet fleet also increased, up 3.7% compared to 2024, with 19,851 unique aircraft flying in July, per WingX.

WingX Managing Director Richard Koe says bears should get out of the way.

He said July 2025 was the busiest in six years.

Koe says:

‘July’s record performance shows real momentum in the business jet market. North America’s 7% growth last week and strong UK summer holiday traffic to destinations like Mallorca demonstrate the underlying strength we’re seeing. Even with some regional variations, the overall trend remains very positive.’

U.S. segments (49,681) were up 7% compared to 2024.

Both Florida (+11%) and California (+10%) saw double-digit year-over-year gains.

Europe flights (13,686) were up 2% compared to Week 31 a year ago.

European private jet segments are up 2% over the trailing four weeks.

| Market | Week 31 | %Change vs. prior week | % Change vs W31 2024 | 52-week high | Week | 52-week low | Week | Last 4 Weeks (Flights) | %Change vs YOY |

| Global | 74,850 | -2% | 5% | 78,808 | 2025-26 | 60,509 | 2025-02 | 305,057 | 2% |

| North America | 51,656 | -1% | 7% | 56,577 | 2024-42 | 42,332 | 2025-27 | 207,208 | 2% |

| USA | 49,681 | -1% | 7% | 54,849 | 2024-42 | 40,714 | 2025-27 | 198,788 | 2% |

| Florida | 4,677 | 8% | 11% | 9,229 | 2025-08 | 4,074 | 2024-32 | 18,080 | 2% |

| California | 4,567 | 0% | 10% | 5,285 | 2025-17 | 3,726 | 2025-27 | 18,147 | 3% |

| Texas | 4,382 | -3% | 5% | 5,916 | 2024-42 | 3,885 | 2025-27 | 18,005 | 4% |

| Europe | 13,686 | -5% | 2% | 15,740 | 2025-28 | 6,313 | 2025-01 | 58,694 | 2% |

| UK | 1,700 | -8% | 3% | 2,217 | 2025-28 | 1,005 | 2024-52 | 7,850 | 2% |

| Germany | 1,191 | -5% | 2% | 1,634 | 2025-22 | 549 | 2025-01 | 5,067 | -12% |

| France | 2,222 | -6% | -5% | 2,814 | 2025-28 | 1,040 | 2024-52 | 9,882 | 2% |

| Switzerland | 767 | 6% | 3% | 1,036 | 2025-04 | 526 | 2024-47 | 3,170 | -1% |

| Italy | 2,179 | -5% | 6% | 2,476 | 2025-26 | 516 | 2025-01 | 9,124 | 9% |

| Middle East | 1,552 | -5% | -4% | 1,776 | 2025-20 | 1,159 | 2025-10 | 6,332 | 5% |

| Africa | 800 | -1% | 14% | 1,047 | 2025-17 | 603 | 2024-36 | 3,228 | 16% |

| Asia | 1,722 | -11% | -15% | 2,587 | 2025-09 | 1,722 | 2025-31 | 7,613 | -6% |

| South America | 2,022 | -6% | 9% | 2,855 | 2025-09 | 1,801 | 2025-01 | 8,705 | 17% |

Source: WingX for Private Jet Card Comparisons. Includes Jets and VIP Airliners.

Fractional and charter operators also saw another positive week.

Their 40,012 segments were up 5% year-over-year.

U.S. fractional and charter operators flew 27,407 segments, up 9% compared to last year.

Florida, with 2,645 segments, was up 17% compared to Week 31 in 2024.

European counterparts, however, were in the red.

Their 9,748 segments were down 3%.

| Market (Part 91K & Part 135) | Week 31 | %Change vs prior week | %Change vs W31 2024 | 52-week high | Week | 52-week low | Week | Last 4 Weeks (Flights) | %Change vs YOY |

| Global | 40,012 | -1% | 5% | 42,159 | 2025-25 | 31,062 | 2025-02 | 163,072 | 2% |

| North America | 28,287 | 1% | 9% | 30,966 | 2024-42 | 23,662 | 2024-35 | 112,970 | 4% |

| USA | 27,407 | 0% | 9% | 30,299 | 2024-42 | 23,012 | 2024-35 | 109,406 | 3% |

| Florida | 2,645 | 10% | 17% | 5,497 | 2025-01 | 2,180 | 2024-35 | 10,060 | 6% |

| California | 2,968 | 0% | 8% | 3,483 | 2024-43 | 2,559 | 2024-36 | 11,927 | 4% |

| Texas | 1,962 | -3% | 8% | 2,845 | 2024-42 | 1,848 | 2025-27 | 8,061 | 6% |

| Europe | 9,748 | -6% | -3% | 11,286 | 2025-28 | 4,649 | 2025-02 | 42,168 | -1% |

| UK | 1,178 | -11% | -2% | 1,595 | 2025-28 | 717 | 2025-03 | 5,614 | -2% |

| Germany | 754 | -7% | -11% | 1,113 | 2025-22 | 417 | 2025-01 | 3,304 | -18% |

| France | 1,574 | -8% | -8% | 2,082 | 2025-28 | 746 | 2025-03 | 7,193 | 1% |

| Switzerland | 567 | 3% | 0% | 799 | 2025-08 | 379 | 2024-47 | 2,338 | -4% |

| Italy | 1,653 | -7% | 1% | 1,874 | 2025-27 | 376 | 2025-01 | 6,916 | 5% |

| Middle East | 850 | -4% | -19% | 942 | 2024-35 | 519 | 2025-10 | 3,406 | -11% |

| Africa | 168 | -19% | -36% | 312 | 2024-52 | 168 | 2025-31 | 824 | -14% |

| Asia | 248 | -5% | -23% | 412 | 2024-46 | 198 | 2025-29 | 956 | -24% |

| South America | 36 | -31% | -14% | 84 | 2025-11 | 27 | 2024-40 | 166 | 18% |

Source: WingX for Private Jet Card Comparisons. Includes Jets and VIP Airliners.

For those of you looking for something negative to focus on, all developing markets saw double-digit declines for fractional and charter operators in Week 31.

Africa segments led the way with a 36% year-over-year drop.

Asia (-23%), the Middle East (-19%), and Asia (-5%) all saw year-over-year declines.

What’s more, Asia (-24%), Africa (-14%), and the Middle East (-11%) were down double digits over the trailing four weeks.

Find the perfect solution for your private aviation needs

Save Time. Buy Confidently.

Receive an apples-to-apples comparison of programs that meet your needs from more than 500 jet card and fractional options covering 65 points of differentiation and over 40,000 data points.